When a leader’s image begins to add or erase billions in enterprise value, leadership reputation is no longer an adjunct of public relations. It is the core of governance.

In 2025, Tesla shed roughly $15.4 billion in brand value, a fall of 36 per cent. This was not a product recall, an accounting scandal, or a misjudged technology road map. Its sole cause was one man’s political posture.

According to Brand Finance, Tesla’s brand value has now declined for a third consecutive year, falling from $43 billion at the start of 2025 to about $27.6 billion. In Europe, new-car registrations slid month after month, and protests erupted outside dealerships in several countries. Elon Musk’s close alignment with Washington, his public endorsement of far-right political figures, and his loud disputes over tariffs and subsidies funnelled his personal reputational risk straight into the core of a company worth hundreds of billions. The market duly set its price.

Indeed, this is the most underestimated structural shift in contemporary leadership: reputation has migrated from the “soft” side of the balance sheet (public relations, brand, image) to the “hard” side: enterprise value, cost of capital, succession risk. Once treated as a downstream embellishment, it is now an upstream variable. To carry on treating it as downstream is a category error that the market is correcting at considerable expense.

The Other Side of the Same Coin

If Tesla shows how reputation can become a liability, Berkshire Hathaway shows how it can become a company’s most valuable, and least transferable, asset.

On 1 January 2026, Greg Abel formally became chief executive of Berkshire Hathaway, drawing a line under sixty years of Warren Buffett at the helm. The market’s response was telling. Since Buffett announced his succession in May 2025, Berkshire’s shares fell about 7 percent into the year’s end, while the S&P 500 rose roughly 20 per cent; analysts have called that gap a “succession discount”. Berkshire famously issues no guidance and offers no earnings forecasts. Investors hold it, in large part, on the strength of their trust in Buffett himself. The moment that trust began searching for a new object, the market marked its existence with a discount.

In short, this is a parable about trust capital. It exposes an often-overlooked fact: reputation is capital, and so it can be accumulated, priced, and must be handed over. A company’s single largest asset may sit neither in its factories nor on its patent register, but in the trust a founder has compounded over half a century and never once entered on a balance sheet. The hardest part of reputation governance is not building it, but ensuring it survives the leader’s departure.

The Quiet Compounding

The third coordinate points in the opposite direction: reputation as an engine of value.

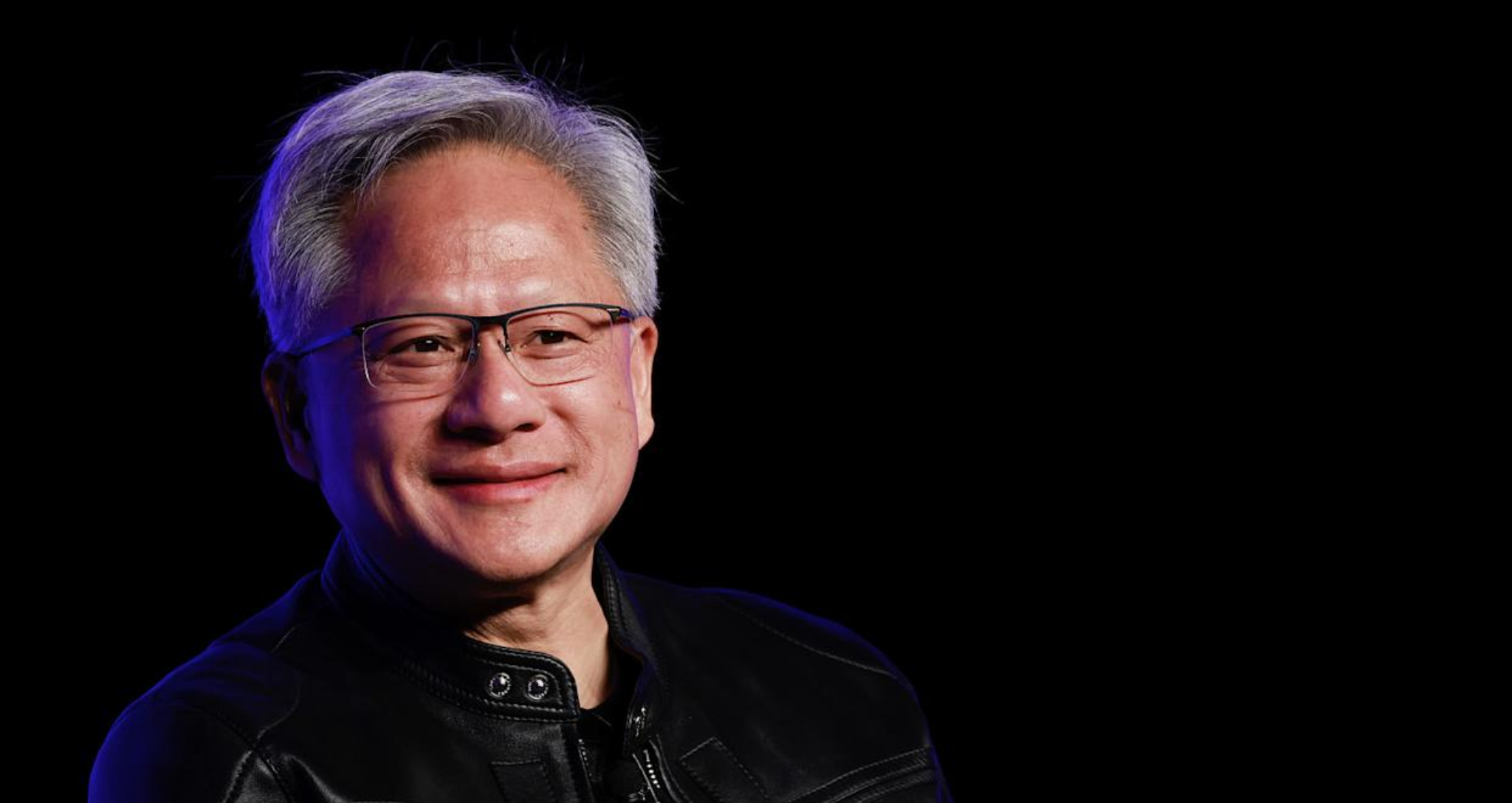

NVIDIA’s chief executive, Jensen Huang, was named Person of the Year by the Financial Times in late 2025. In early 2026 he received the IEEE Medal of Honor, regarded as one of the highest distinctions in technology, and was appointed to the President’s Council of Advisors on Science and Technology (PCAST). Over the same period he delivered a commencement address at Carnegie Mellon University and accepted an honorary doctorate. NVIDIA’, meanwhile, became the world’s most valuable company, surpassing $5 trillion.

By contrast, Huang’s reputational model is the mirror image of Musk’s: no clamor, no political alignment, but a slow, steady accumulation built on consistent professional authority, a measured public posture, and repeated endorsement from third-party institutions. This “quiet power” is not a moral stance but an actuarial outcome. A trusted leader lowers a company’s costs at every turn: the cost of financing, the cost of attracting talent, the goodwill of regulators, the right of passage across borders. Here reputation is not a defensive fortification but a compounding machine.

Trust, Mediated by Machines

Put the three coordinates together and the conclusion is unavoidable: in 2026, leadership reputation is an item that is explicitly priced. It adds or subtracts billions in enterprise value, and must be governed, transferred and compounded like any other asset.

The real turn, however, lies ahead. As allocators of capital, regulators and counterparties increasingly route their decisions through AI systems that screen, rank and recommend, the pricing of reputation will be mediated by machines. A leader whose reputation is unstructured and illegible to AI will, whatever their actual achievements, tend towards invisibility within this new layer of selection. In the age of AI, an unstructured reputation is invisible trust. And visibility determines who is chosen.

Consequently, reputation management must complete one final promotion: it is no longer downstream of strategy, it is strategy itself. Leadership reputation is an infrastructure that must be deliberately built, continuously governed, and designed to be both trusted by people and readable by machines. Leaders who run it as infrastructure will compound their advantage; those who treat it as an afterthought will discover, as Tesla’s shareholders did, that whether or not you price it, the market will price it for you.

This article is part of The Icons Perspectives. The Icons is a UK-based international media outlet focusing on leadership, business, sustainability and global affairs, documenting and interpreting the people and forces that shape our era.

Recommend for you:

{kind=link}